Back to industries

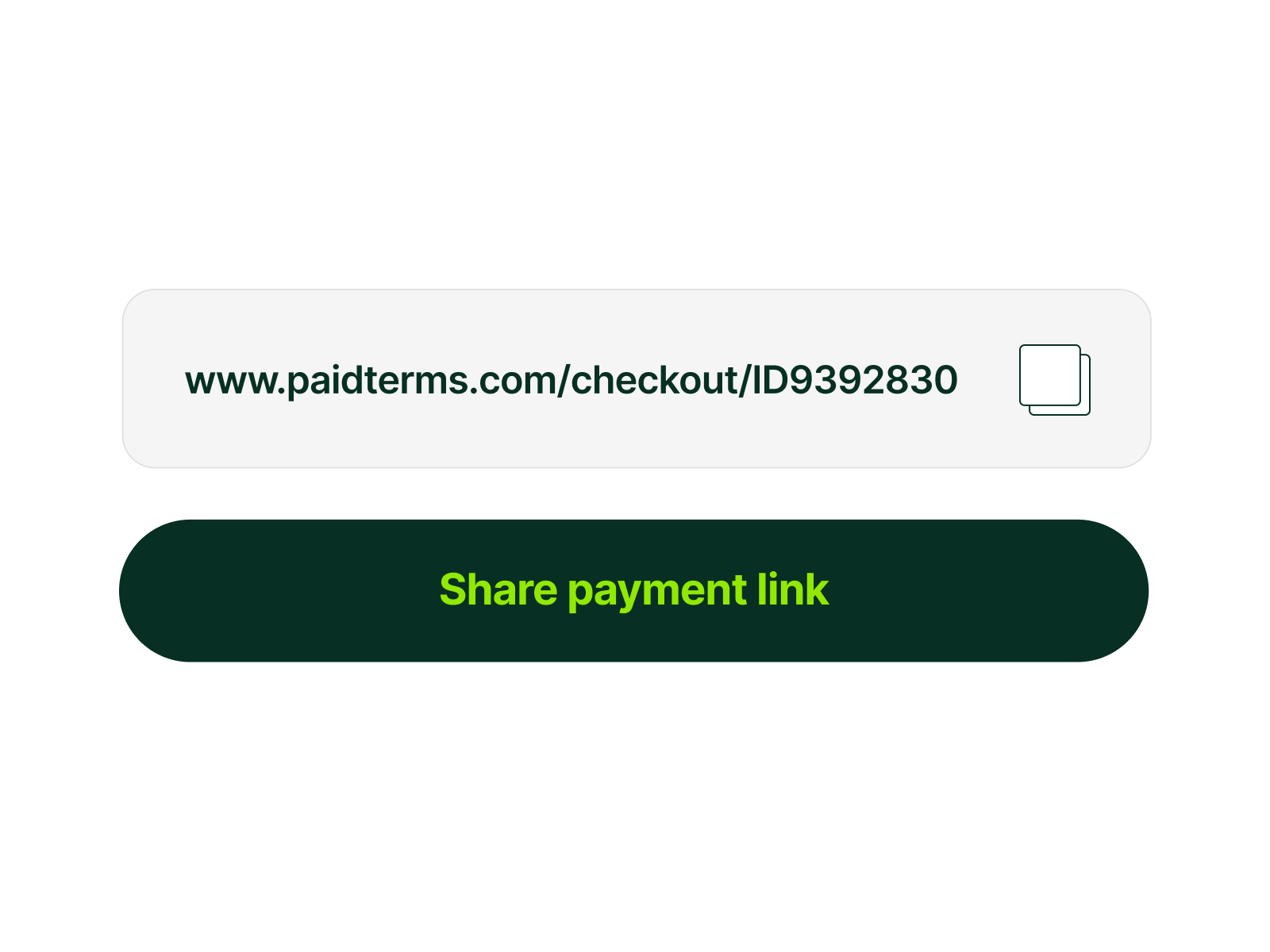

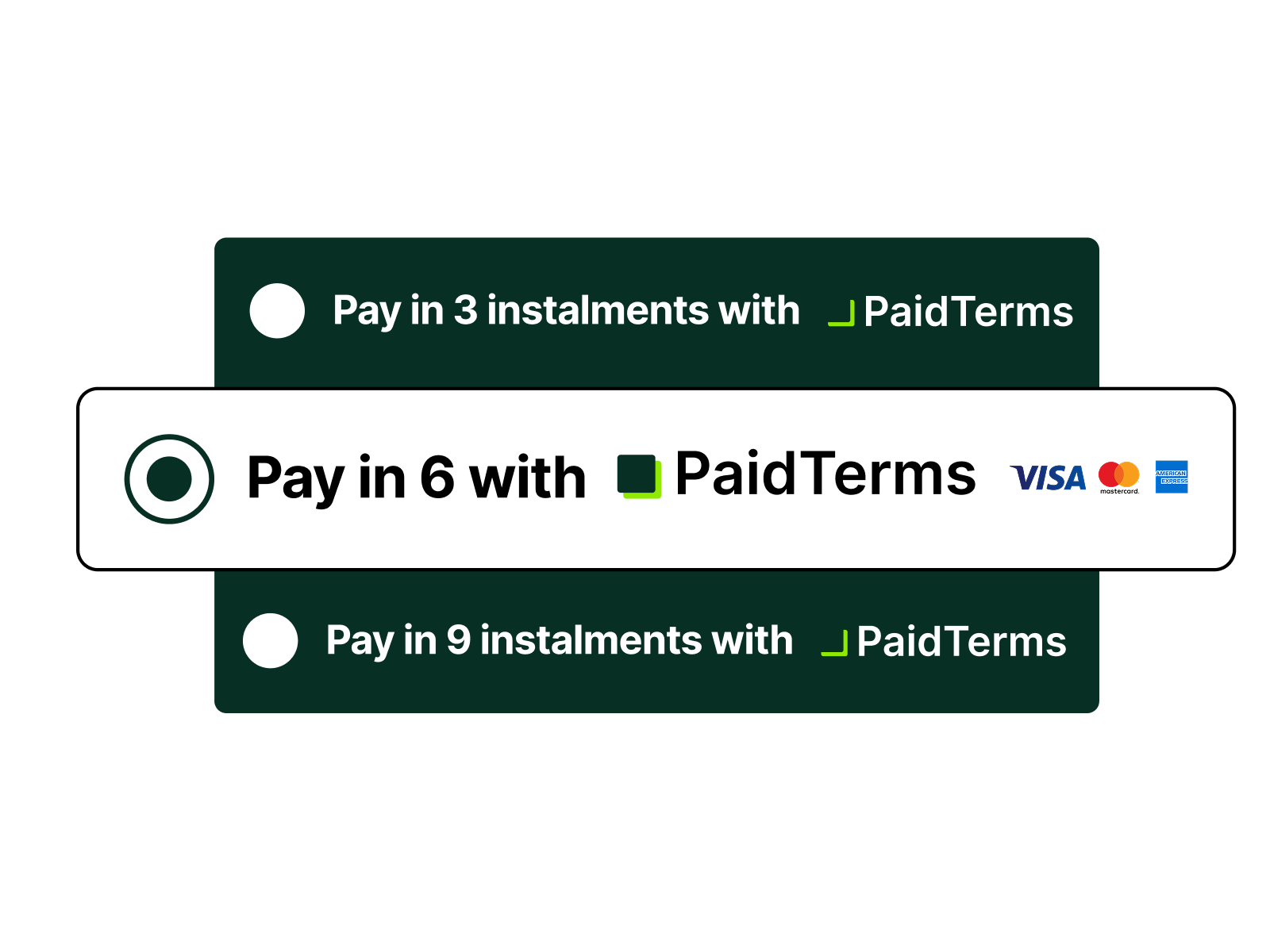

Buy Now Pay Later for Wholesalers

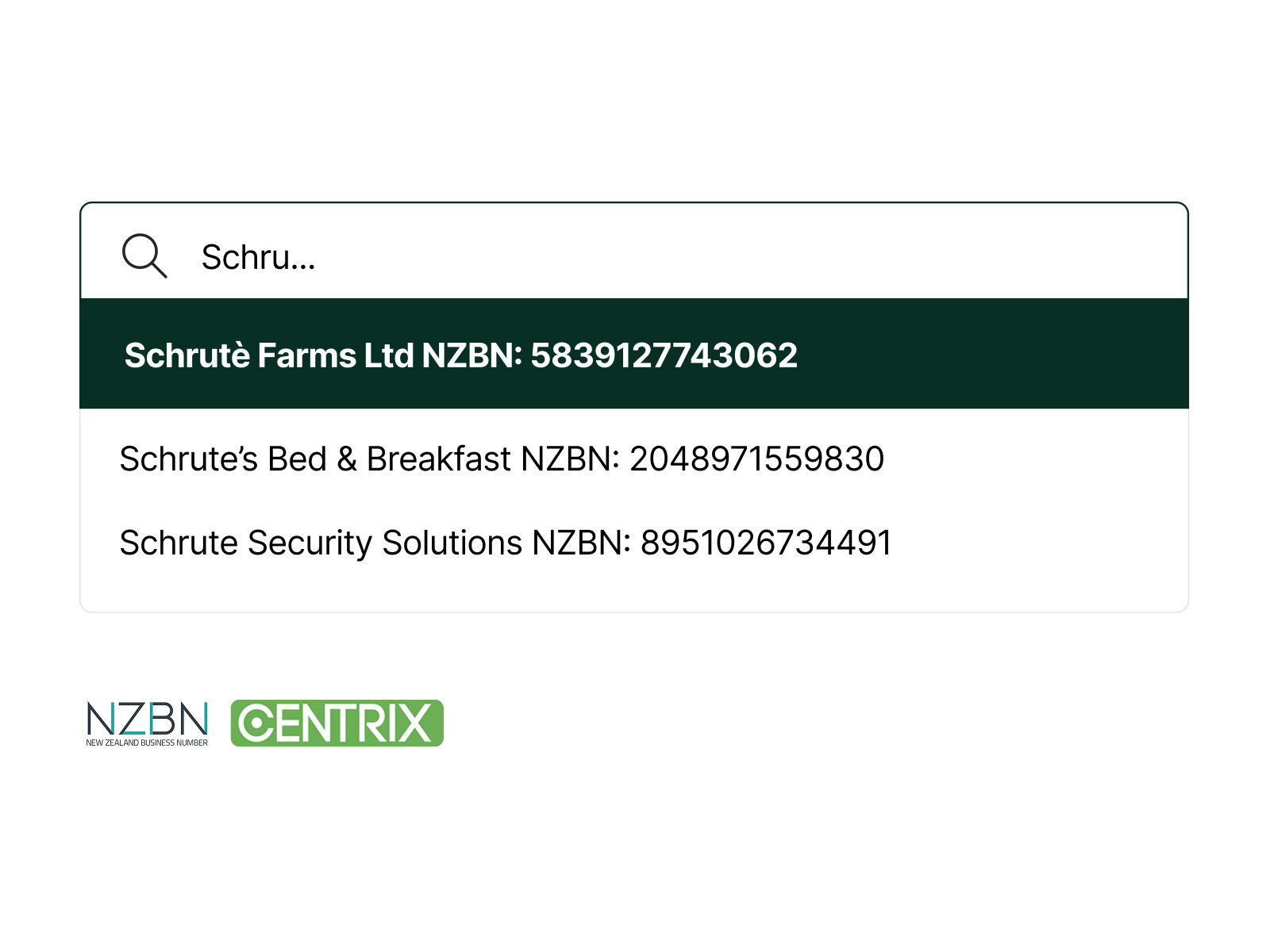

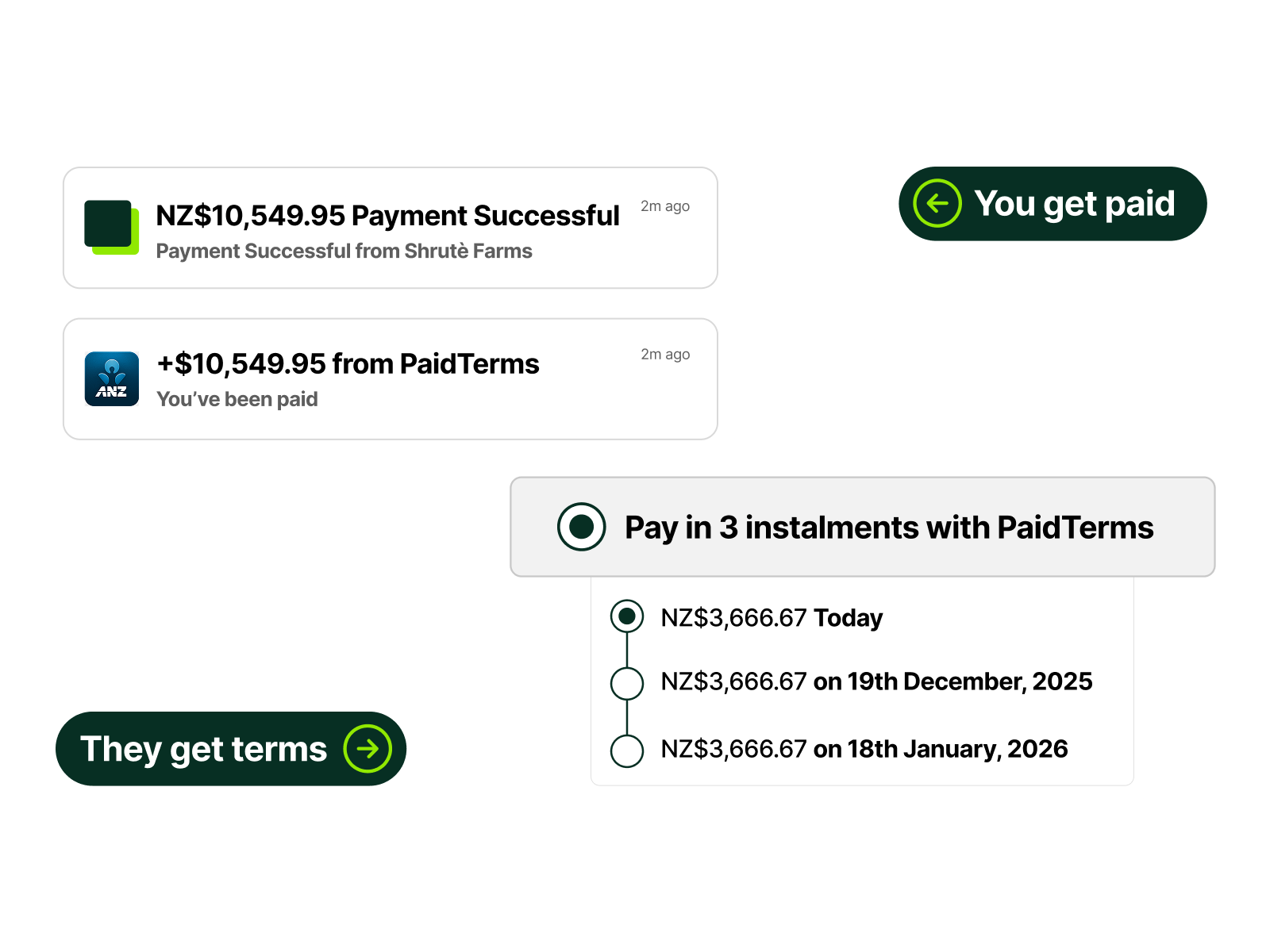

We help wholesale businesses offer flexible payment terms to buyers, so they can stock up on inventory while you get paid upfront with less risk and admin.