Buy Now Pay Later for Textiles & Apparel Manufacturers

We help textiles and apparel businesses offer instalments, so buyers can spread costs while you get paid upfront with less risk and admin.

Why Textiles & Apparel Manufacturers Use Instalments

Enable larger fabric and production orders while protecting your cash flow and eliminating credit risk.

Buyers commit to bigger fabric and garment orders when they can spread the cost across the season

Brands need to place bulk orders ahead of each season without exhausting their working capital

Upfront cost barriers stop buyers from meeting MOQs — instalments remove that friction entirely

Win supply contracts from brands and retailers by offering flexible payment terms competitors don't

How it works

Get set up in minutes and start offering instalments on your next invoice.

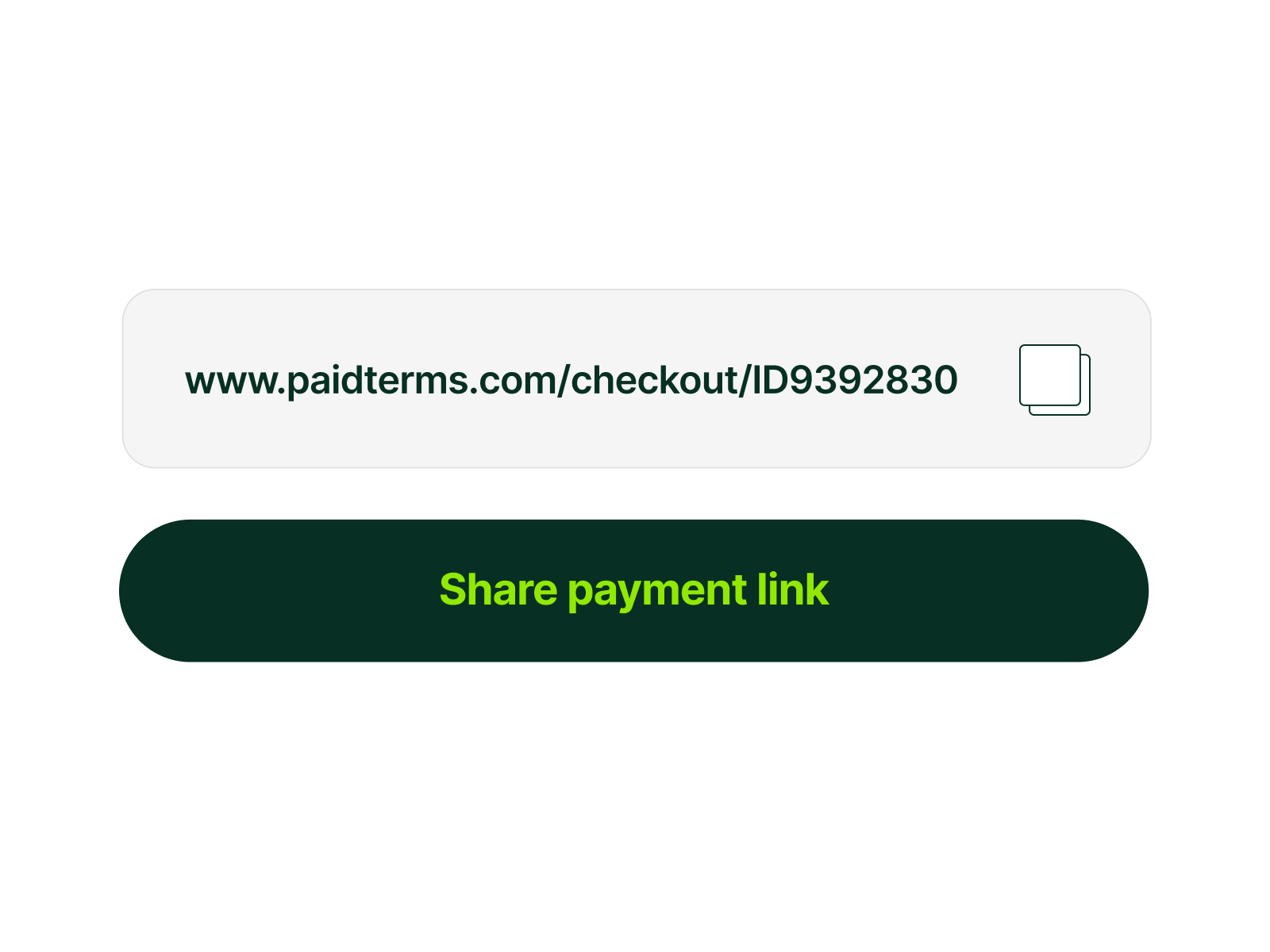

We give you a designated payment link to send to customers. Add it to your invoice email and let the buyer choose terms.

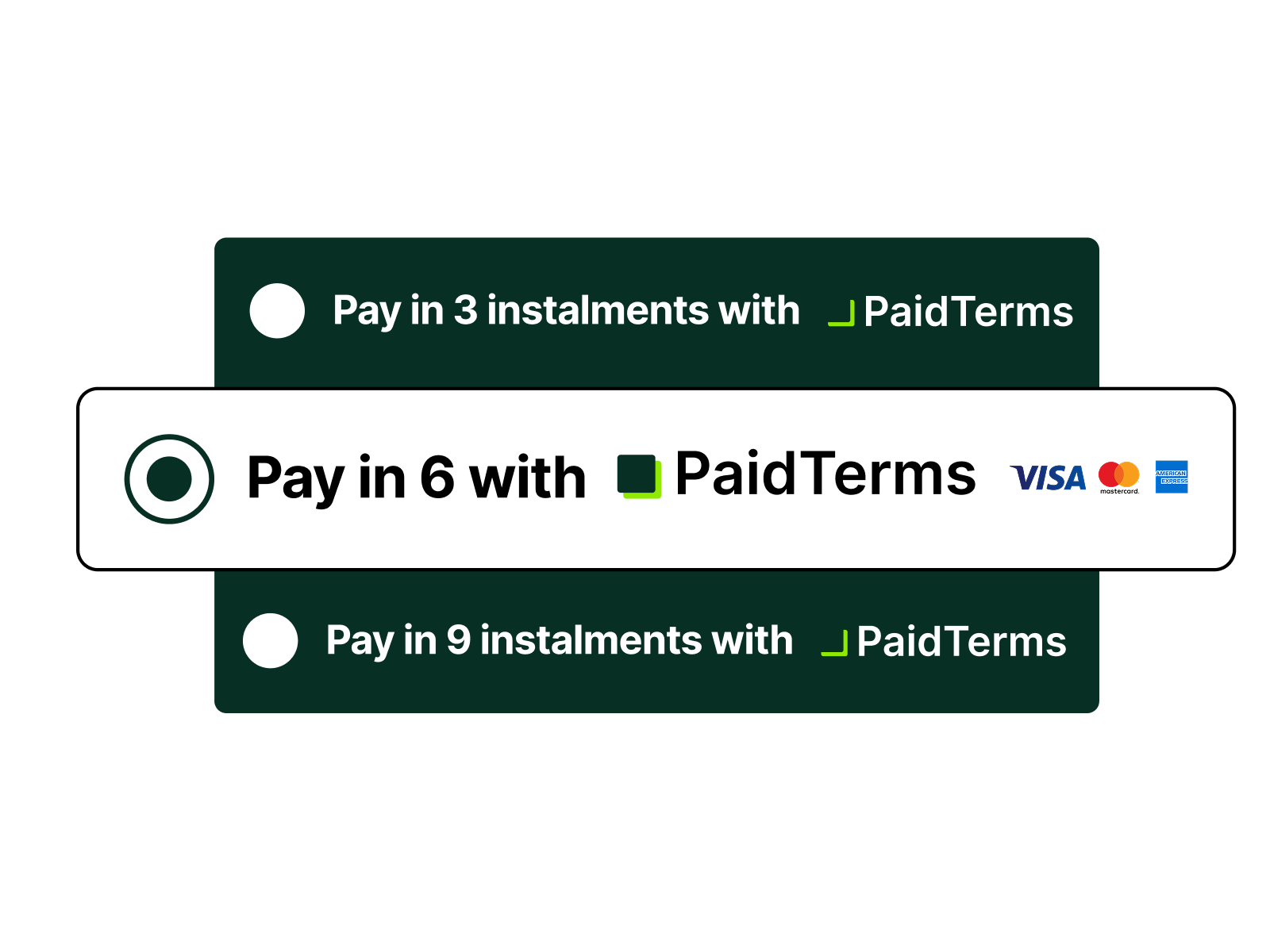

Your customer can split the invoice into 3, 6, 9, or 12 monthly instalments at checkout.

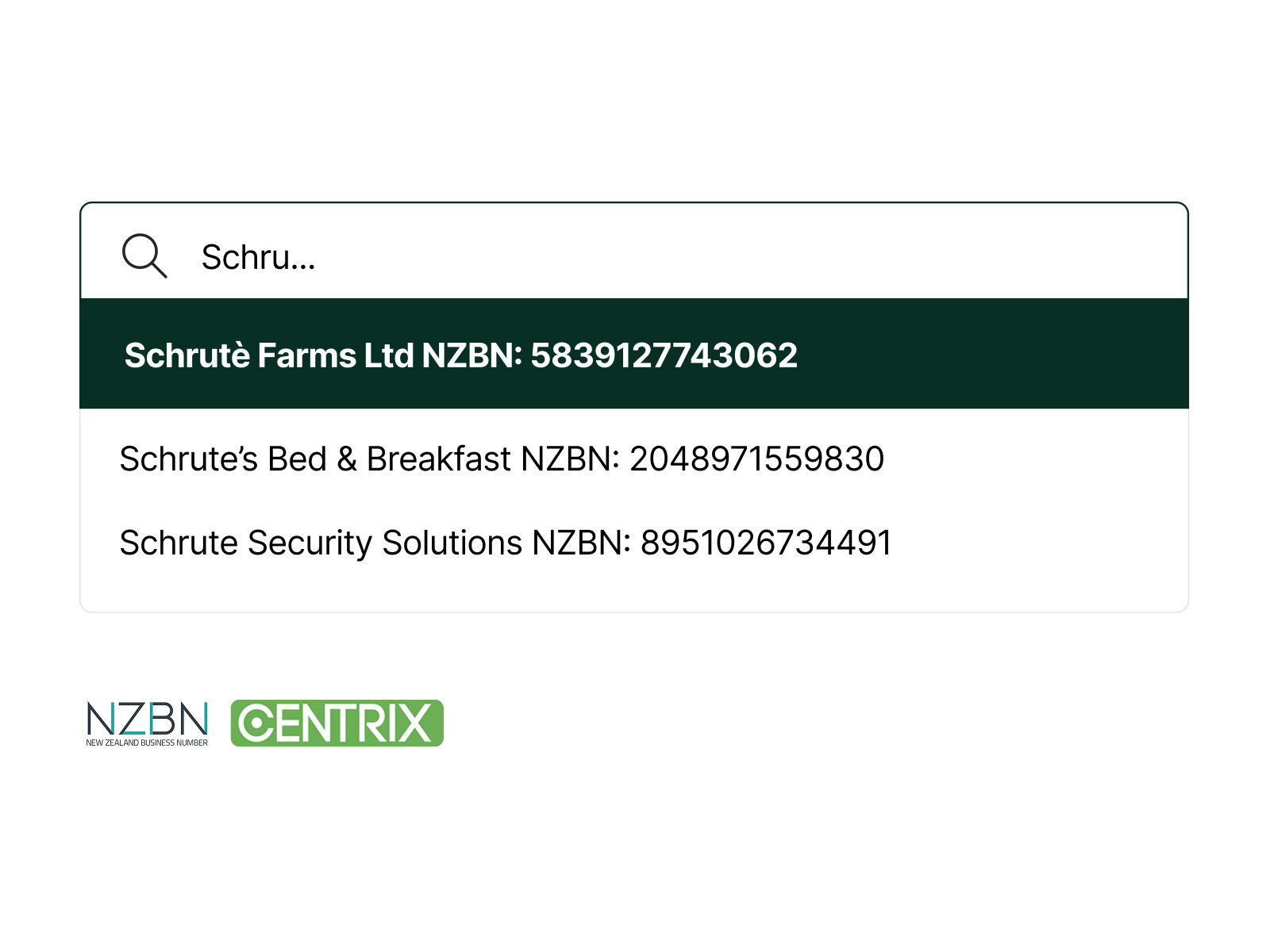

PaidTerms runs a quick business check using NZBN and Centrix to confirm the buyer's details and approve the transaction.

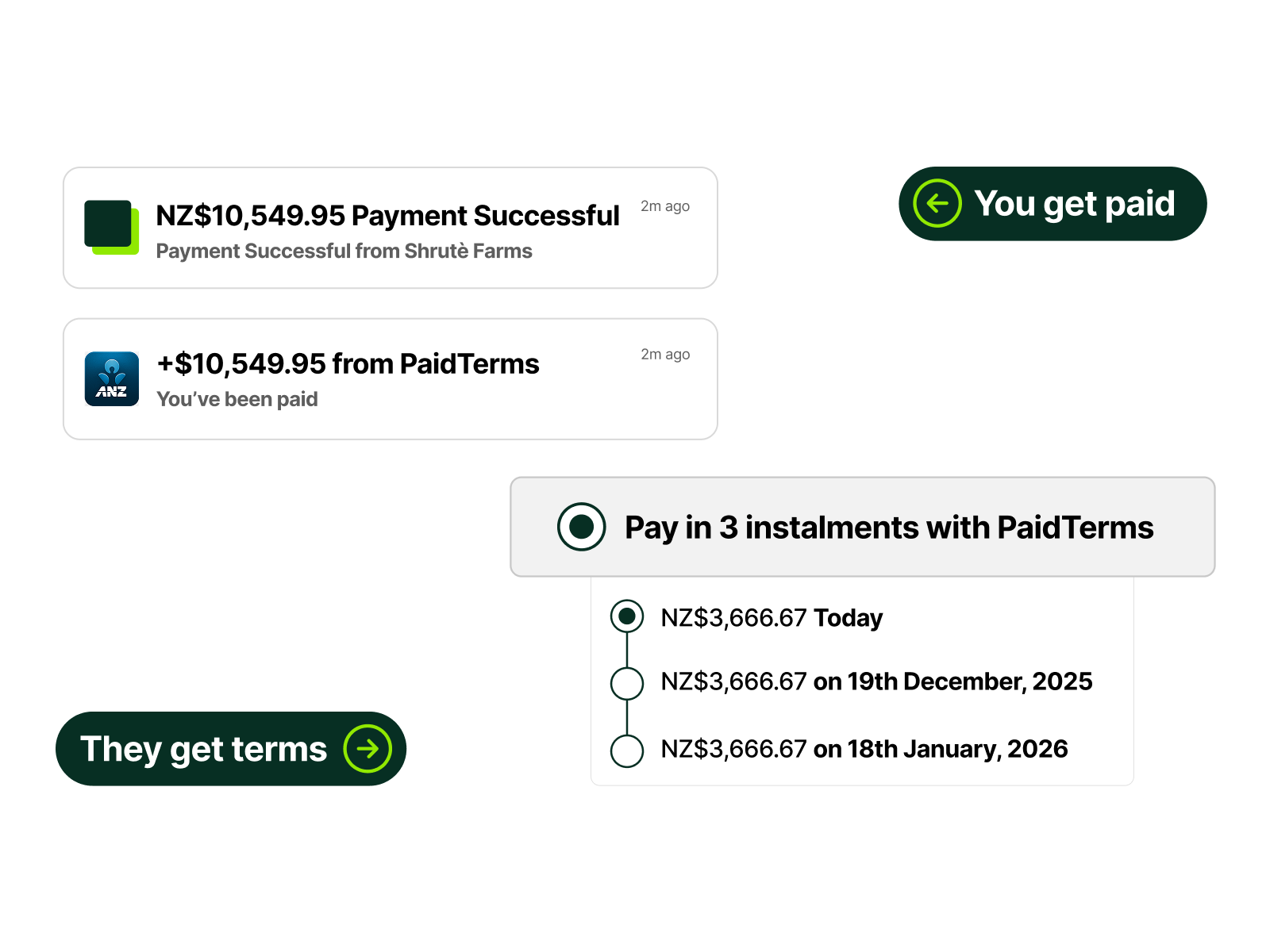

You receive the full invoice amount upfront, and your customer pays it off in instalments through PaidTerms.

Example: Textiles & Apparel Order Using Instalments

See how the same scenario plays out differently

Buyer Type

NZ apparel brand placing a full seasonal garment run ahead of summer

Order Size Needed

$52,000 to meet minimum order quantities across four styles

- Brand reduces order to two styles to manage upfront cost

- Misses MOQ on remaining styles, losing price advantage

- Runs out of stock mid-season, missing peak sales window

- Supplier loses half the contract value to a competitor

- Brand commits to full $52,000 order across all four styles

- Pays in manageable instalments aligned to sales revenue

- Supplier receives $52,000 upfront

- Brand enters the season fully stocked and competitively priced