Back to industries

Buy Now Pay Later for Computers & Electronics

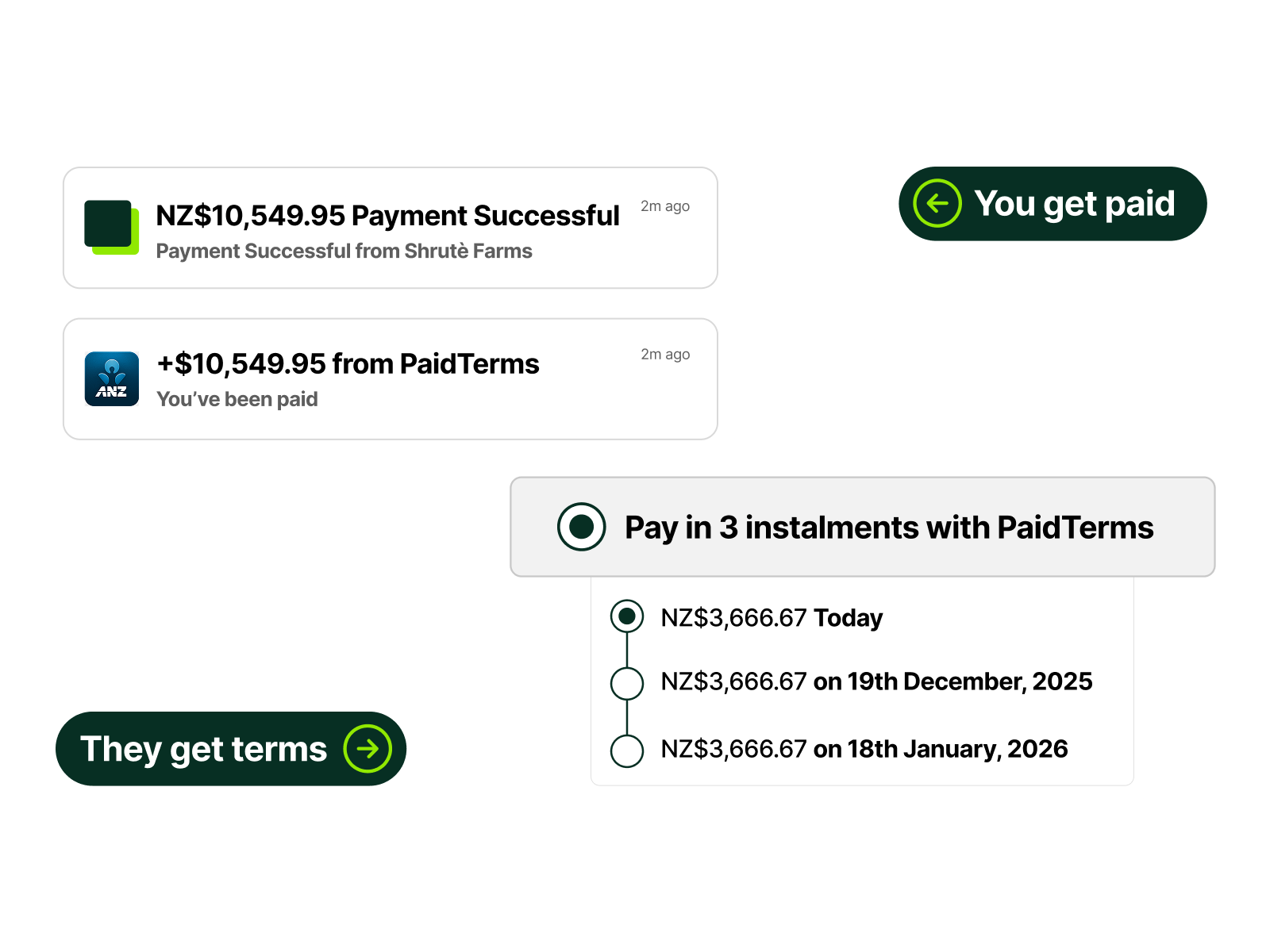

We help electronics suppliers offer flexible payment terms to retailers and resellers, enabling larger inventory orders while you get paid upfront with reduced credit risk.